What are rates and why do we pay them?

Rates are a property tax paid by households and businesses. There are two different types of rates in Northern Ireland, domestic rates for residential properties and non-domestic rates for businesses and other non-residential properties, such as hospitals and schools.

The total revenue raised through domestic and non-domestic rates in Northern Ireland is approximately £1 billion a year. This money supplements the Executive’s budget and supports public service provision in Northern Ireland, such as hospitals, schools and roads, and directly funds work carried out by district councils, e.g. refuse collection and street cleaning.

Domestic and non-domestic rates consist of two elements:

- the regional rate; and

- the district rate.

Regional rate

The Northern Ireland Budget 2016-17 explains the purpose of the regional rate:

The regional rate, which is determined by the Executive, generates additional resources to support those central public services that are the responsibility of the Executive.

Regional rate revenue is unhypothecated, which means the Executive can use it to fund any project.

The regional rate is usually determined and set annually by the Northern Ireland Executive, through an Order under powers conferred by Article 7(1) and (3) of the Rates (Northern Ireland) Order 1977 (as amended), subject to affirmative resolution by the Northern Ireland Assembly.

For 2016-17, the Executive set the domestic regional rate at 0.4111 pence in the pound; and the non-domestic regional rate was set at 32.40 pence in the pound.

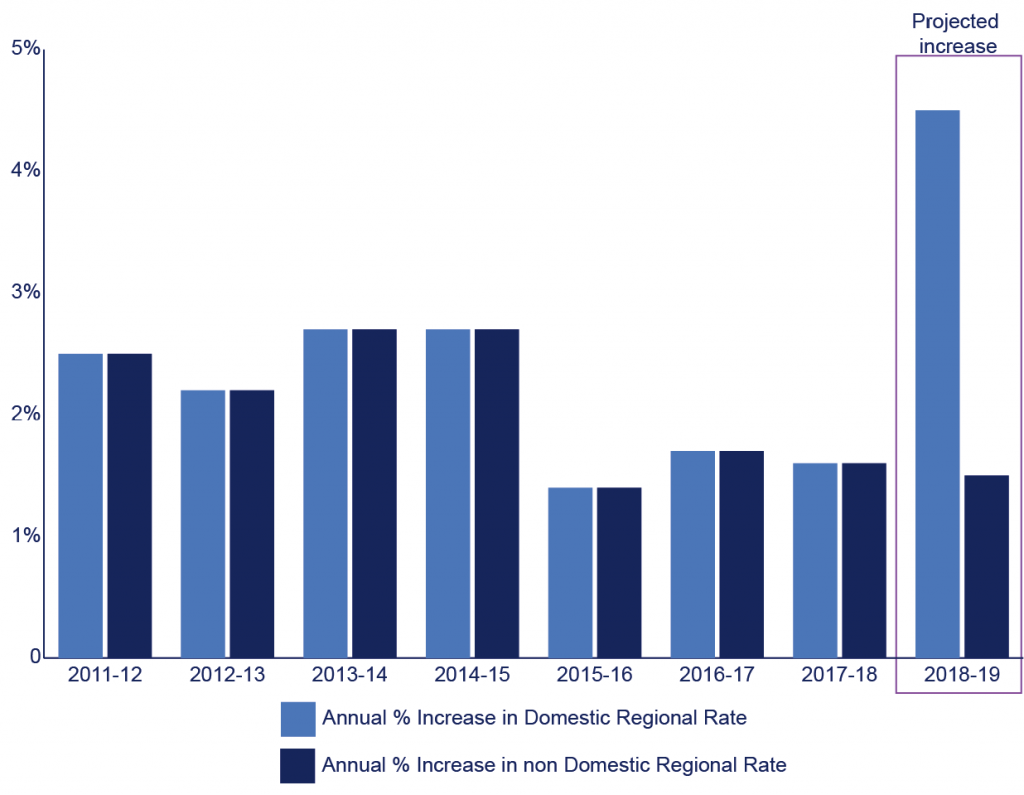

For 2017-18, due to the absence of a fully functioning Executive, the Northern Ireland regional rate was set by legislation in Westminster, via the Northern Ireland (Ministerial Appointments and Regional Rates) Act 2017. This set the domestic regional rate at 0.4177 pence in the pound and the non-domestic regional rate at 32.92 pence in the pound, following the policy trend since 2011 – see Figure 1.

However, for 2018-19, with the Executive still not functioning, the Secretary of State proposes to depart from this policy approach – see Figure 1 and discussion below. In a Written Statement to the House of Commons, she said:

As part of setting a budget, it is essential that the UK Government provides clarity on the regional rate. This budget position has been constructed on the basis of an increase in the domestic regional rate of 4.5%. I consider that this is a necessary and important step to continue to support public services, particularly in health and education. The non-domestic rates would rise only at 1.5%, in line with inflation.

The Government introduced a fast-track Northern Ireland (Regional Rates and Energy) Bill on 21st March 2018 which, if enacted, will set Northern Ireland’s regional rate for the 2018-19 financial year.

District rate

The district rate is similar to the regional rate in that it is split between domestic and non-domestic ratepayers. However, the district rate is set annually by individual district councils, not the Executive. Moreover, the revenue raised goes directly to the ratepayers’ district council to fund local services in the council area, not to the Executive to fund Northern Ireland-wide services.

District rates for 2018-19, published in February, show Lisburn and Castlereagh to have the lowest domestic (0.2969 pence) rates with Fermanagh and Omagh having the lowest non-domestic (21.3348 pence) rates. The highest district rates are in Derry City and Strabane, (0.4683 pence) for domestic and (30.0353 pence) for non-domestic.

Rates bills are calculated in the following way:

Domestic rates bills

Domestic property is assessed by the Land and Property Services (LPS) on the basis of its capital value, i.e. the amount a domestic property reasonably could have been sold on the open market using 1st January 2005 market prices. Valuations then are put on a list as specified under The Rates (Capital Values, etc.) (Northern Ireland) Order 2006.

The calculation for 2017-18 is:

Capital value of property x (domestic regional rate + domestic district rate)

E.g. a domestic property in Mid Ulster District Council with a capital value of £100,000: £100,000 x (0.004177 + 0.003126) = £730.30

Non-domestic rates bills

Non-domestic property in Northern Ireland is assessed on the basis of its Net Annual Value (NAV).

The NAV is based upon an assessment of the annual rental value that the property reasonably could have been expected to let for on the open market on 1st April 2013, as specified under the NAV List (Time of Valuation) Order (Northern Ireland) 2013.

LPS is currently revaluing all non-domestic properties in Northern Ireland and new valuations will come in to effect on 1st April 2020 based on rental values as at 1st April 2018.

The calculation for 2017-18 is:

NAV of property x (non-domestic regional rate + non-domestic district rate)

E.g. a non-domestic (business property) in Mid Ulster District Council, with a NAV of £100,000: £100,000 x (0.329200 + 0.235369) = £56,456.90

Following the above calculation, relevant deductions are made to the final bill for applicable allowances, such as Freight and Transport Relief, Small Business Rate Relief and Industrial De-rating.

Regional rate and the Northern Ireland budget

Regional rates revenue is one of the funding sources available to the Executive, beyond block grant allocations from Westminster. Since 2011 the Executive has annually increased the rate for regional rates in line with inflation. The Budget 2016-17 explains the rationale for this policy:

Since 2011 the Executive has agreed that both the domestic and non-domestic Regional Rate should be uplifted in line with inflation. This was established because the Executive was mindful of not imposing undue additional burdens on households in the difficult economic climate that prevailed at the time. The Executive’s 2016-17 Budget is once again predicated on the continuation of this policy, with overall revenues from both the normal domestic and non-domestic Regional Rates being held in line with inflation. This, alongside the decision not to implement water charges, helps Northern Ireland maintain the lowest household taxes in the UK.

The Executive’s document goes on to argue that this contributes to a lower tax burden on households and businesses, thus leading to increased consumer confidence. Increasingly, questions have been asked about the prudence of this approach, given the financial arrangements under devolution, including the Executive’s restricted fiscal powers.

As noted earlier, the Secretary of State’s proposed 4.5% regional rate increase departs from the Executive’s past approach in this area. Figure 1 below shows this potential change, illustrating the annual percentage increases from 2011 to date.

As mentioned above, the regional rate is a key element in calculating bills for both domestic and non-domestic rate payers. Consequently, the increase in the regional rate beyond the level of inflation – as introduced in the Westminster bill – is expected to increase domestic ratepayers’ bills in 2018-19.

This departure breaks with the Executive’s past established approach on a devolved matter, which, since 2011, had been increasing the regional rate in line with inflation. Questions naturally arise as to why now?