What is ‘outcomes-based budgeting’, and what are the key benefits and limitations of using it?

Outcomes-based budgeting may be defined as:

The practice of developing budgets based on the relationship between funding and expected results. It increases visibility into how government policies translate into spending and focuses on the outcomes of a funded activity i.e. the quality or effectiveness of services provided.

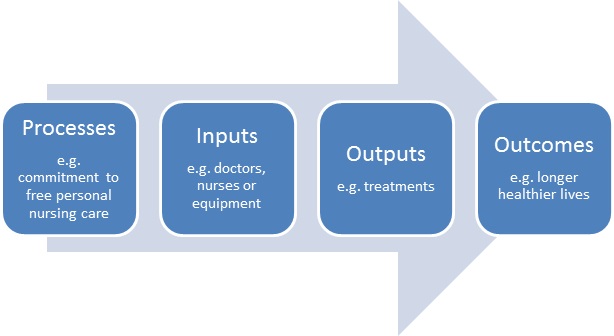

Fundamental to understanding this type of budgeting is the difference between outputs and outcomes:

- Outputs – the goods and service that governments produce or provide.

- Outcomes – the impact or consequences of the outputs for the community.

Its aim is to align programmes and services with prioritised government outcomes. In this regard, the Children and Young People Committee of the National Assembly for Wales commented:

…[T]here are very few promises, programmes or policies that any government can deliver without backing them up with money…For things to happen, well-meaning words and assurances usually have to be followed through with cold hard cash.

Therefore, budgets could be viewed as a tangible expression of a government’s priorities, performances, decisions and intentions.

The Northern Ireland Assembly’s Committee for Finance and Personnel stated that there should be ‘clear, visible linkages between Budget allocations and the Programme for Government’. In response, the Department of Finance and Personnel (DFP) indicated that past attempts to link funding with targets had had limited success.

Key Benefits

Transparency and participation

One benefit of outcomes-based budgets is increased transparency and participation in the budget process. It enables stakeholders to identify linkages between funds allocated and proposed outcomes. In this way, stakeholders can recognise whether the stated outcomes have been achieved. One group of academics link the two themes of transparency and participation. They state that the absence of transparency between funding and targets has a detrimental effect on participation.

Around the world, civil society organisations have begun analysing government budgets to identify their impact on social programmes. This type of analysis enables them to successfully lobby for programme changes, to benefit both funders and programme users.

Accountability

Another benefit of outcomes-based budgeting is improved accountability of the Executive, to the Assembly and the public. Clear linkages between funding and outcomes help to measure the effectiveness of intervention programmes. It also assists in clarifying the roles and responsibilities of politicians and civil servants in achieving identified priorities.

Highlights government spending inefficiencies

The transparency afforded by outcomes-based budgeting enables stakeholders to see results from budget objectives and to identify mechanisms by which they are/are not achieved. Stakeholders can assess for themselves whether funds expended on achieving a particular outcome provided value for money. Some academics have suggested that greater transparency of costs, resources and performance has encouraged government agencies to restructure budgets, reduce spending and better align budget resources with performance.

Outcomes-based budgets are collaborative in nature, helping to promote coordination and cooperation between departments and agencies, which in turn makes inefficiencies easier to identify.

Improved stakeholder services

Such budgeting also can be used as a management tool, to evaluate programmes and services, and thereby facilitate cost-effective use of public money. As one academic noted, it can be used by policymakers when articulating government’s goals and objectives and monitoring progress.

Academics further suggested that outcomes-based budgets integrate funding and objectives – budget and performance – enabling managers to focus on economy, efficiency and effectiveness, making performance measurement an integral part of budgeting.

Key Limitations

Additional costs

In the 2012 Committee for Finance and Personnel report on the Response to the Executive’s Review of the Financial Process in Northern Ireland, stated that the mapping of targets to funding may not be a ‘practical or even efficient use of resources’. The additional analysis to assign funding to outcomes may result in additional costs and add confusion to the budgeting process[1].

Identifying outcomes

The number of government-identified outcomes may be problematic. Academics note that governments often introduce large numbers of outcomes that can dilute the usefulness of the available data and discourage stakeholders from using them.

[1] See paragraph 35, page 14 of the report.