Later this month, the new Minister of Finance will announce the outcome of the Executive’s June Monitoring Round. But what is a Monitoring Round, and what opportunities does it present for the Assembly to scrutinise the Executive’s management of public money?

What is a Monitoring Round?

The In-year Monitoring process gives the Executive a mechanism for reviewing spending plans and priorities during the year, in light of the most up-to-date financial information.

Why have In-year Monitoring?

- It is a formal process that allows departments and their Ministers to address in-year financial issues at three Monitoring Rounds each year: June, October and January.

- It allows for changes in Executive priorities to be reflected in additional allocations.

- It allows the Executive some flexibility to meet emerging needs when circumstances change.

The Assembly votes to approve departmental expenditure limits through the Supply Procedure, Budget Bills and the Estimates. Assembly Members may therefore expect to be fully informed about the way the Executive alters those limits.

What happens during In-year Monitoring?

Executive departments:

- must give up any ‘reduced requirements’;

- may ‘bid’ for additional funding;

- may propose ‘proactive reallocations’ of their own budgets to meet higher priority pressures; and,

- may propose ‘reclassifications’ of budget from one expenditure category to another, subject to restrictions.

The restrictions include:

- The ‘category’ assigned to the expenditure. For example, capital funding cannot be used for resource/current expenditure.

- When below the current ‘de minimis threshold’ of £1 million, the department does not need approval for reallocations, subject to (1) HM Treasury ringfence; and, (2) Executive ringfence.

- Extra flexibility is given to the Department of Health.

Details of the process are outlined in annually updated guidance issued by the Department of Finance.

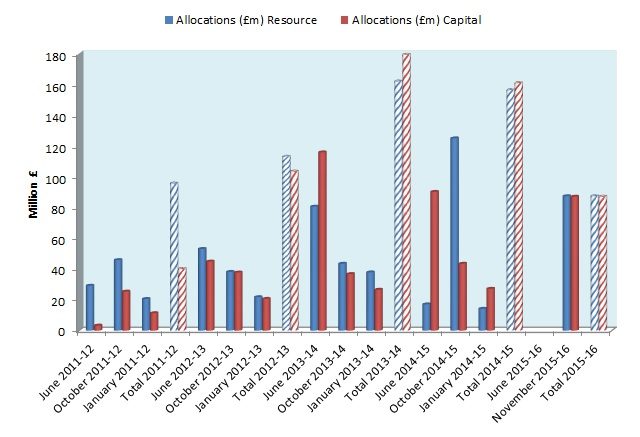

In-year Monitoring allocations during the last Assembly mandate

Figure 1 shows the funding (both Resource Departmental Expenditure Limits (DEL) and Capital DEL) allocated through the In-year Monitoring process.

In total, nearly £1.2 billion was allocated through In-year Monitoring during the 2011-16 period. This is a significant amount of resources, which underlines the importance of Assembly scrutiny.

Opportunities for Assembly scrutiny

Following each Monitoring Round, the Minister of Finance usually makes an oral statement to the House. On occasions however, the outcome of a Monitoring Round has been released through a written Ministerial statement. These statements are published on the Department of Finance website. But the Assembly is not asked to approve the re-allocations, it is merely informed of them. This means that its main avenue for scrutiny is through its statutory committees.

The Department of Finance’s guidance states:

Assembly Committees have an important role to play in the scrutiny of departmental spending plans. For that reason, departments must ensure that they engage fully with their Assembly Committees in respect of the In-year Monitoring process. The extent and timing of this engagement is obviously a matter for individual Committees. However, there should be early engagement with Committees in order to establish their requirements. The Department of Finance recommends that Committees should be kept informed of financial matters on an ongoing basis. (page 30)

Committees can expect therefore, to receive briefings on bids, reduced requirements and internal reallocations from their respective departments. In 2014, the Research and Information Service’s Public Finance Scrutiny Unit (PFSU) conducted a detailed study of the bid documentation submitted by departments as part of the In-year Monitoring process.

The key findings of the PFSU study were that there was:

- Some inconsistency in adherence to the rules;

- An unclear relationship between bid priority and success; and,

- An unclear relationship between bid compliance with requirements of In-year Monitoring guidance and success (i.e. provision of information about the linkage to Programme for Government targets, or equality/poverty impacts).

It seems likely therefore, that there is some scope for committees to encourage departments to improve the quality and openness of their In-year Monitoring processes. For example, departments could be encouraged to provide copies of their draft bid documents before they are submitted to the Executive for consideration. This would enhance the transparency of public expenditure in Northern Ireland. In particular, it could make it easier for the Assembly to see the linkage between the money allocated and the outcomes delivered under the Executive’s Programme